Did you know that the 2010s is the only decade since the mid-1800s that didn’t have a recession? Recessions are part of the economic cycle we all experience. The key is learning how to recession-proof your client’s portfolios so that they don’t experience true financial hardships when the market takes a dip.

The Bucket Plan® simplifies this as it does with the rest of the holistic financial planning process. Using cash-flow based financial planning and concepts like the money cycle and risk assessments, you can communicate with your clients better and put their minds at ease about what the future holds.

The market will always have fluctuations, but with a bit of pre-planning on the front end, you can set your clients up for success regardless of what’s happening on Wall Street.

Building a Recession-Proof Retirement Strategy with the Bucket Plan

The Bucket Plan methodology is used to create an individualized comprehensive financial plan for your clients. This three-bucket approach to holistic financial planning segments the client’s money based on the time expectations of when they will need it.

Flight-to-safety is a recession-proof market trend that occurs when investors sell off higher-risk investments to invest in safer products that are backed by the government. In bear markets, investors often transfer their funds out of equities and into government securities and money market funds.

Flight-to-safety is often accompanied by a demand decrease for assets backed by private agents. Clients exchange lower profits for less risk when there is considerable fear in the marketplace.

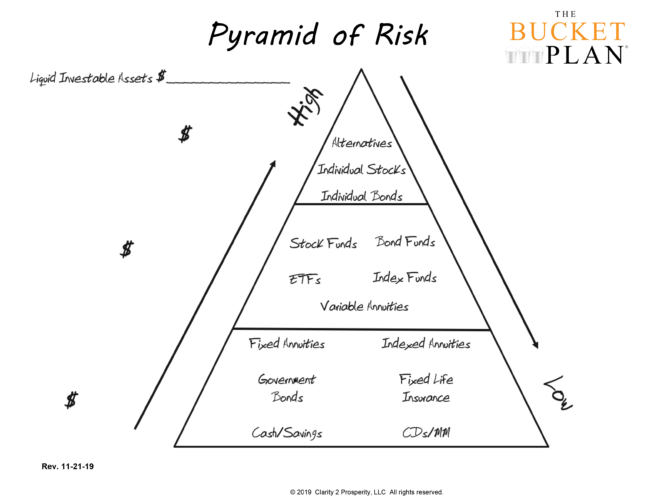

Building a Strategy Around Your Clients’ Risk Tolerance

A holistic financial plan is different from any other investment strategy because it is based on both internal and external factors—including dips in the market, risk tolerance, job loss, birth of a child, death of a spouse, change in marital status, etc. It considers how the client’s objectives will continue to evolve and works to recession-proof each phase of their life and retirement.

The client’s risk tolerance is the amount of risk that they are comfortable with compared to how much risk they must face to reach their retirement objectives.

Make sure your clients understand that there will always be times of market volatility, and they shouldn’t react emotionally to downturns. Making drastic changes to investments in the client’s Bucket Plan in response to market dips can affect their ability to out-earn inflation, making for a less favorable retirement fund.

There are times when adjustments need to be made to the client’s Bucket Plan. If their risk tolerance changes significantly, you should sit down with them to re-evaluate what their recession-proof retirement plan will look like.

Listen to the latest episode of The Bucket Plan On-Demand Podcast!

How the Bucket Plan Helps Assist in Flight-to-Safety

Flight-to-safety occurs when the client prefers to buy bonds and sell stocks to diminish the potential losses that they would incur during times of market crisis.

Flight-to-safety refers to an abrupt change in investment behaviors during a time of economic disarray where clients sell riskier assets in lieu of more conservative options. A distinguishing aspect of flight-to-safety is the investors’ inadequate risk-taking behavior, which can disrupt credit and other financial markets.

The Bucket Plan has been defined, refined, and tested to provide a recession-proof retirement.

- The Now Bucket contains easily accessible funds for planned and unexpected expenses in the first few years of retirement. This bucket achieves minimal returns that likely will not keep pace with inflation, so don’t overfill it.

- The Soon Bucket is for the first ten years of retirement plus a hedge for inflation. The client will need this money sooner rather than later, so invest it conservatively to offset the client’s increased cost of living in retirement. This mitigates the risk of withdrawing at a market low, as you should not expose this account to extreme market fluctuations.

- The Later Bucket is designed to house investments for long-term growth in the later stages of retirement. Long-term investments are more aggressive because the client has more time to cover any potential losses.

Become a Bucket Plan Certified Financial Advisor

The Bucket Plan Certified® designation is a FINRA-recognized professional designation, which indicates to clients that you have elevated your skillset to that of a truly holistic advisor, delivering a best-interest planning process and a holistic financial plan.

The Bucket Plan accounts for the client’s income needs, time horizon, volatility tolerance, and tax situation for a one-of-a-kind, product-agnostic, recession-proof financial plan.

Advisors are required to have a bachelor’s degree or at least two years of industry experience, a life insurance license, and must hold at least one of the following:

- CPA

- CFP®

- ChFC®

- Series 6

- Series 7

- Series 65

- Series 66

Earn up to nine hours of Continuing Education (CE) credits for Certified Financial Planners and up to nine hours of CE for insurance professionals (depending on the state) with The Bucket Plan® 1.0.

To learn more about how to recession-proof your clients’ portfolios, talk with one of our business development representatives today!

Prosperity Capital Advisors provides more than just investments. Are you looking for solutions to simplify and solve the complex challenges and opportunities you face as an investor every day? Prosperity Capital Advisors is committed to looking at the big financial picture and providing congruent and holistic services to you.

Financial Professional Use Only

The information provided in this presentation is not intended as investment advice or legal advice. The information provided is for informational and training purposes only. The information in this presentation was accurate as of the time of the material was created. Tax laws and rulings can frequently change. Please discuss the client’s current situation with an accountant or tax advisor.

")