")

Talking About Life Insurance

We like to pretend we are going to live forever. Most of us would rather do just about anything other than think deeply about our own death. That’s why effectively positioning life insurance to clients is particularly challenging.

Nobody wants to ponder their own mortality. But the reality is that we will all die at some point, and most of us want our loved ones to be well taken care of when that time comes. That’s why selling life insurance is such an essential part of holistic financial planning. You have to learn how to talk to clients.

Selling life insurance is a very personal venture—you are discussing delicate and painful topics.

When positioning life insurance to your clients, focus on the beneficiaries. People primarily buy life insurance to cover end-of-life expenses and care for their surviving family members.

Why a Plan is Not Holistic Without Life Insurance

The Bucket Plan Process is foundational to holistic financial planning and everything we do at C2P Enterprises—including life insurance.

Most Insurance Marketing Organizations (IMO) focus on gross production and sales from their agents and advisors. But we concentrate on client solutions that are in their best interest. We mitigate risk for clients by helping advisors incorporate our best-interest approach in case design, product selection, and implementation of insurance solutions as financial planning tools.

Clarity Insurance Marketing is a best interest-focused insurance marketing organization that specializes in screening, selecting, and supporting top-quality fixed insurance products. Their award-winning services cover fixed and indexed annuities, single premium and traditional life insurance, and asset-based long-term care products.

Clarity Insurance Marketing works with holistic advisors committed to representing the client’s best interests. As such, almost all affiliated advisory practices have either a Registered Investment Advisor (RIA), Investment Adviser Representative (IAR), or registered representative of a broker-dealer in their office to help represent life insurance as a part of a holistic financial planning solution. We mitigate risk for institutions, advisors, and American families nationwide.

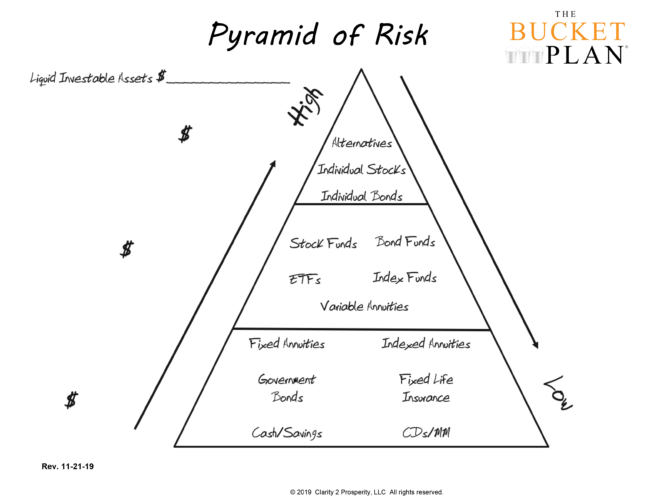

To better understand their needs, take each client through the Pyramid of Risk, discern their volatility tolerance, and measure their tax bracket.

It’s crucial that you stay up-to-date on the fast-paced and ever-changing life insurance industry. Study your clients. Try to understand their challenges and goals, so you can find a product that fits their needs.

Once you know what the client expects from a life insurance policy, you can introduce products to help them achieve their goals.

Structuring the Conversation of Life Insurance with Your Customer

Positioning life insurance to a 20-year-old is very different than selling life insurance to a 60-year-old. But no matter who you are working with, you should be able to ask questions like,

“If you died tomorrow, would your family be able to pay their bills and continue their current lifestyle?”

Financial advisor client communications should begin by educating them on the difference between term and permanent life insurance, including the advantages and disadvantages of each.

Term life insurance is one of the most popular types because of its simplicity and low premiums. These policies are great for healthy young clients who can secure reasonable rates and use the savings to invest in other securities, but they only pay out if the policyholder dies during the policy period.

For example, term life insurance is better for people ages 25-45. They are typically working through life events like buying a home, getting married, growing their families, or saving for college. They usually have a lower net worth than older age groups and higher debt-to-income ratios.

“Term is like renting an apartment. Permanent is like buying a house. When you rent an apartment, you are building no equity, but it’s generally cheaper. When you buy a home, you’re going to pay more, but you get equity in return. With term life insurance, you have a liability, but no asset to show for it.” –Dave Alison, CFP®, EA, BPC

Learn more about The Bucket Plan Process and positioning life insurance to your holistic financial planning clients.

Financial Professional Use Only

The information provided in this presentation is not intended as investment advice or legal advice. The information provided is for informational and training purposes only. The information in this presentation was accurate as of the time of the material was created. Tax laws and rulings can frequently change. Please discuss the client’s current situation with an accountant or tax advisor.