Key Takeaways

- The six months following April 15 may offer more planning leverage than any other period of the year.

- One Big Beautiful Bill Act provisions are creating tax cliffs that do not show up in any single line item. They only become visible when you have the full tax return in hand.

- The order of assets, meaning which accounts clients draw from during their lifetime and what gets left behind, has the potential to significantly increase what a family keeps.

Every year, without fail, I get a call around December from a client who wants to talk tax planning.

These are not clients who have not heard from me. They have. We had the conversation. But there is something about December that finally makes it feel urgent, and by the time it feels urgent, most of what we could have done together is no longer available. The year’s income is set. Capital gain distributions have been announced. The window has mostly closed.

That gap between when the planning work can make a difference and when clients feel motivated to engage with it is one of the defining challenges of proactive tax management. It is also exactly why May matters so much.

What Many Advisors Are Missing About Midyear Tax Planning

I co-presented a webinar with Ed Slott and his team. We designed the session around a problem we both see consistently across practices of every size: many advisors are not running a proactive tax management process at all. Annual optimization at best.

And in too many cases, clients in their 60s with large IRAs are simply being told to wait until RMDs force their hand at 73 (or 75 for those born in 1960 or later), leaving up to 15 years of low-bracket capacity sitting unused.

The advisors who deliver the most value have built a process that starts the moment April 15th passes, when the planning runway is longest and the opportunity to act is greatest.

Here is what top advisors are doing to stay ahead.

Request Tax Returns Before the Planning Window Closes

The moment April 15th passes, our team at Prosperity Capital Advisors starts requesting completed tax returns from every client. We upload them into Holistiplan and treat them as a roadmap, a detailed record of every variable that shaped last year’s tax outcome and a jumping-off point for what we can do differently this year.

Then we layer in everything we know from the custodians:

- How much income has already come out of IRAs this year

- What our capital gain budgets look like

- What dividends and income we can expect from post-tax portfolios through December

From that foundation, we build a pro forma tax projection of the opportunities available over the next five or six months.

Why This Year Is Different

This year’s returns carry something no prior year has. These are the first returns showing how the One Big Beautiful Bill Act (OBBB) provisions flow through a client’s tax picture, and what many clients are seeing does not match what they expected going in.

Nobody likes a large tax bill. But what clients genuinely dislike is a surprise tax bill, which is what tax management is designed to mitigate.

That’s why we start the planning process now, rather than in November when most of the year’s variables have already been determined. That’s what separates proactive tax management from reactive year-end scrambling.

[Related: The One Big Beautiful Bill Act (OBBB): Key Tax Changes Advisors Should Know]

Map the OBBB Interactions Before Your Clients Feel the Cliffs

One of the most widespread misconceptions we have encountered around the 2025 return involves Social Security. The “no tax on Social Security” narrative that circulated widely in the media was never accurate.

What changed under OBBB was the enhanced senior deduction. For some clients, their Social Security income is exactly what pushed them over the income threshold to lose it. One provision appeared to give, and another took it away.

This is the nature of OBBB. Its provisions do not create problems in isolation:

- The SALT cap increase from $10,000 to $40,000

- the new $6,000 per-person senior deduction

- The change to itemized deduction limits at higher income levels

These all carry different thresholds and different phase-out ranges, and they interact in ways that only become visible in the aggregate. Clients without proactive advisors in 2025 may have missed bracket capacity they did not know they had.

The goal now is to make sure that does not happen again in 2026.

What to Consider Building into Your Projections

Here are two items worth building into forward projections now that will not appear on the 2025 return at all:

- New automatic charitable deduction for non-itemizers ($1,000 single, $2,000 married filing jointly)

- Reduction in the benefit of itemized deductions at the 37% bracket, where the effective deduction benefit is now 35%.

On the simplification side, under OBBB, modified adjusted gross income now equals adjusted gross income for most clients without foreign income exclusions. Previously there were more than ten different MAGI definitions.

That alignment makes projecting income thresholds for the new provisions considerably more straightforward.

[Related: Year-End Tax Strategies for High-Net-Worth Clients: OBBB Planning Guide]

Ask Who Inherits Before Deciding How Much to Convert

When a client asks whether they should consider Roth conversions, I start with two questions.

- “What direction do you think tax rates are going?” Hopefully they answer “up” because then we’re on the same page.

- “Who are the cast of characters? Where does this money go when you are gone?”

If the answer is charity, Roth conversions may not be the priority. Charitably inclined clients may be better served giving from their IRAs first.

Thanks to the SECURE Act’s elimination of the stretch IRA, traditional IRAs can be among the least tax-efficient assets for wealth transfer, but they may be among the best assets to direct to charity, because the charity pays no tax on the distribution.

It is also worth reviewing client wills for cash bequests, since estate attorneys focused on legal structure rather than tax planning may have written bequests payable from after-tax assets. For clients with large IRAs, directing charitable gifts from the IRA and letting beneficiaries inherit the step-up-in-basis assets instead has the potential to meaningfully increase what heirs receive.

If the money is going to children or grandchildren, the cast of characters matters considerably, and the conversation extends well beyond federal tax rates.

Here’s a Real-Life Example

I worked with a client in her early 90s with a large IRA who was considering whether to convert. When I asked about her children, one was a surgeon in New York City and the other was in tech in San Francisco.

Both were in the highest federal brackets and in two of the higher state tax brackets in the country. And where was she? Texas, with no state income tax.

The potential state tax arbitrage, converting in her hands at her effective rate rather than leaving those distributions to her children at theirs, changed the entire framing of the conversation.

How many beneficiaries will split the account is just as important. A large IRA divided among several lower-income heirs may create far less per-person compression under the SECURE Act’s 10-year rule than the same balance left to one or two high-income children forced to liquidate it within a decade on top of their existing income.

Modeling the inheritance scenario alongside the owner’s retirement income plan is what allows advisors to give a reasoned, individualized recommendation rather than a generic one.

[Related: Year-End Charitable Giving Strategies: A Guide for Financial Advisors]

Start the Roth Analysis Now and Executing in December

There is an important distinction between when to begin the Roth conversion conversation and when to act on it.

We start the analysis early in the year, especially if markets are volatile. We build the pro forma projection, map out bracket capacity, and model what converting at different levels could mean over a client’s lifetime and for the beneficiaries in the cast of characters conversation.

We also look at where clients fall within what Ed Slott calls the ‘sweet spot,’ the window between age 59½ and 73 (or 75 for those born in 1960 or later), with no early withdrawal penalties and no RMD requirements. Clients in their 60s with large IRAs may have up to 15 years in that window.

Ed calls the failure to use that window the minimum mentality. The M in RMD stands for minimum, not maximum. Advisors who treat the minimum as the target are effectively telling clients to leave years of low-bracket capacity on the table.

The better question is not how little is required to come out of the IRA, but how much can strategically come out while rates are known and brackets are favorable.

As Ed put it during our webinar:

“Every year that goes by that you don’t maximize the low brackets, 12%, 22%, 24%, they’re gone. They’re wasted. The tax break on blowing a low bracket, even one year, is lost forever.”

The End Goal

The goal is not to eliminate the traditional IRA entirely. Maintaining enough balance to take advantage of standard deductions, low brackets each year, and QCDs for charitably inclined clients is part of the strategy. The pro forma projection is what determines how much to convert and when.

We continue to refine our strategy in Q4. Mutual fund capital gain distributions are not finalized until then, and one unexpected large distribution can meaningfully alter a client’s bracket position. Build the plan now. Complete execution at year end with complete information.

For clients already subject to RMDs, there’s one coordination point that matters considerably. RMD dollars cannot be converted to Roth. The full RMD must be satisfied across all IRA accounts before any conversion can occur, and all IRAs are aggregated for this purpose.

Advisors who do not hold all of a client’s IRA assets need to confirm the full RMD has been satisfied across every institution before initiating a conversion.

[Related: 4 Types of Roth Conversion Strategies to Manage Taxes]

Model the Surviving Spouse Scenario While There Is Still Time to Act

One of the planning conversations I see most consistently overlooked for married clients involves what happens when one spouse passes. And the cost of missing it tends to compound.

When one spouse dies, the survivor files as a single filer with essentially the same income but half the bracket capacity. Under current 2026 tax rates, $400,000 of taxable income puts a married couple filing jointly at roughly the 24% federal bracket. That same income for a single filer falls at 35%.

That is a meaningful ongoing tax increase for the rest of the surviving spouse’s life.

For clients who hold the majority of their assets in pre-tax accounts, covering that larger tax liability often means taking larger IRA distributions. Larger distributions generate more tax. More tax requires more distributions.

It becomes a cycle that is very difficult to exit once it begins, what I call the IRA death spiral.

How to Survive the Spiral

In the year a spouse passes, the final joint return may represent the most significant Roth conversion opportunity in that family’s planning history. Going all-in on conversions in that final joint return year is a substantial tax event.

But as Ed Slott framed it in our webinar: this tax will be paid.

The question is:

- Who pays it

- At what rate they paid it

- Whether their advisor helped them model the surviving spouse scenario and act on it through strategic Roth conversions or asset reordering while the window was still open

Midyear, with the prior year’s return in hand and a full projection built, is when this scenario can and should be modeled for every married client carrying significant pre-tax assets.

[Related: Three Hidden Tax Problems in Your Clients’ Traditional IRAs]

Plan for Lifetime Taxes, Not Just This Year’s Return

All of this—the process, the pro forma projection, the cast of characters conversation, the investment structure decisions, the surviving spouse scenario—only delivers value if the client acts on it.

And getting your client to act is often the bigger hurdle.

Taxes are not intuitive. The default instinct for many clients is that deferring tax equals saving money, because they are focused on today rather than on lifetime taxes or what their beneficiaries may face when inheriting a compressed IRA distribution schedule during their peak earning years. Left to that instinct without a proactive advisor pushing back, they will defer indefinitely.

We are in the behavior modification business as much as we are in the tax management business, and that is especially true right now.

Clients are logging in, seeing new market highs, feeling comfortable with their balances, and feeling no urgency to act. But every dollar of market growth inside a traditional IRA may add to the future tax liability alongside the balance.

As Ed Slott describes it, a traditional IRA functions like a joint account with the IRS, and Uncle Sam is a special kind of joint owner who gets to determine his share based on when the money is needed most or when it is forced out in RMDs.

The number looks good on the statement. The potential tax obligation may be growing at the same rate.

Why It’s More Important Than You May Know

Clients want this conversation more than advisors may realize.

At a conference Ed Slott and I attended recently, a panel of high-net-worth investors were asked what they want less and more of from their advisors. Less email. More phone calls. Specifically, more conversations around tax planning.

“We know how to make money,” one panelist said. “We want help keeping it.” Another asked the room directly: “What am I paying 1% for?” Then she answered her own question: if she were getting good tax advice, she’d pay because she needed it.

The conversation your clients most want is the one that starts right now, in May, with their 2025 return in hand and a process built around using it well.

[Related: How to Provide Exceptional Wealth Management for High-Net-Worth Individuals]

Build This into Your Practice Through The Tax Management Journey®

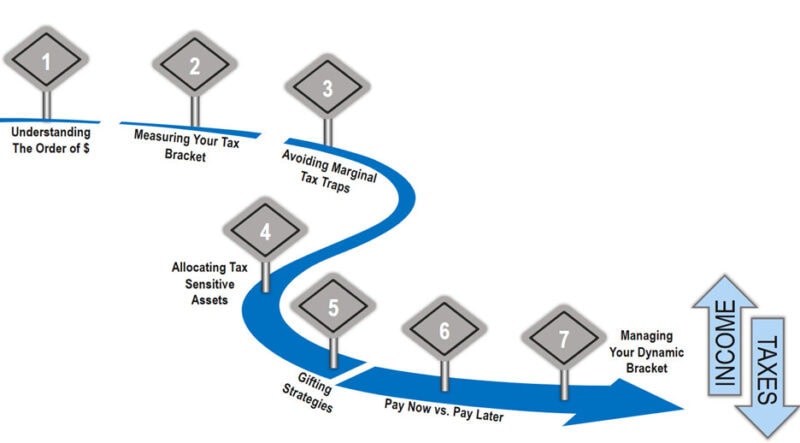

We teach advisors how to execute this kind of midyear planning systematically through The Tax Management Journey® training.

The Tax Management Journey® provides the tools to integrate The Tax Trilogy into your practice:

- A seven-step, repeatable tax management framework

- Pro forma projection processes you can run at the start of each planning cycle

- Visual tools to help explain bracket shifts, Roth conversion trade-offs, and multigenerational tax scenarios in client meetings

- CPA coordination processes to align tax, legal, and planning work

Book a complimentary 20-minute strategy call to explore how this framework may help you implement proactive midyear tax management and work toward attracting higher-net-worth clients. Learn if you qualify to attend the full training at no cost.

Frequently Asked Questions About Midyear IRA and Tax Planning

During our webinar with Ed Slott, several questions came up consistently. Here are some of the most relevant ones for building a midyear tax planning process.

How do I decide how much to convert in a given year?

Start with the pro forma projection. Map out income already realized year-to-date, IRA distributions, capital gains, and dividends, then estimate what is still expected through December.

Identify how much bracket capacity may remain at the 12%, 22%, and 24% levels and size the conversion around that. Review and finalize the plan in Q4 as the client’s full year financial picture plays out. One large unexpected distribution can meaningfully change the math.

Should a client forgo the senior deduction to do more Roth conversions?

For many large-IRA clients who are strong conversion candidates, converting into the 24% bracket and conceding the $6,000 senior deduction may deliver greater long-term benefit. The deduction is capped at the 22% bracket, with a maximum potential tax savings of roughly $1,320 per filer.

Individual circumstances vary. Run the scenario both ways on the pro forma before making a recommendation.

How do QCDs factor into midyear planning?

For clients over 70½ who make charitable gifts, qualified charitable distributions from the IRA can be a tax-efficient option, as the amount comes out without flowing through adjusted gross income.

For clients under 70½ who are charitably inclined, funding a donor-advised fund as a bridge may help bundle deductions in a single year rather than spreading smaller gifts across several years, with a transition to QCDs at 70½.

For any client with large IRAs and charitable bequests written into their will, the conversation may be worth having about directing the IRA to charity and letting beneficiaries inherit the more tax-efficient assets instead.

Can clients still do Roth conversions after RMDs begin?

Yes, but it tends to become more costly. RMD dollars must be distributed first and cannot be converted. The full RMD must be satisfied across all IRA accounts before any conversion can occur.

This is one of the reasons the planning window before RMD age carries significant value, and why allowing those years to pass without a deliberate strategy may prove costly over time. Advisors who do not hold all of a client’s IRA assets need to coordinate across institutions to confirm the full RMD has been satisfied before initiating any conversion.

What is the difference between tax planning and tax management?

Tax planning identifies the opportunity. Tax management is the ongoing process of executing it, adjusting as a client’s income, family situation, and the tax code evolve, and staying ahead of changes rather than reacting to them.

All these laws are written in pencil, and what may be even more variable than the laws is the client’s life: income changes, goals shift, family dynamics evolve.

Tax management means building a process that accounts for all of it, year after year, rather than running a one-time analysis and filing it away.

Learn More: Tax Management Podcasts and Resources

Hear how top advisors are implementing midyear tax management strategies in their practices. Explore real-world insights on Roth conversions, bracket management, and working with clients who have large IRAs:

- The Bucket Plan® On-Demand — Episodes covering tax-efficient distribution strategies and lifetime income planning.

- Rainmaker Multiplier On-Demand — Strategies to help you enhance your advisory firm and overall business model.