What are the 4 Types of Roth Conversion Strategies?

Did you know that the correct Roth conversion strategy can have a significant impact on how much your clients will pay in taxes over the course of their lifetime? Taking advantage of the tax benefits provided by Roth conversion strategies can save your clients on taxes, putting more money back into their retirement.

Roth accounts offer tax-free income in retirement without required minimum distributions. When determining the taxation of Social Security benefits or if higher Medicare premiums apply, it isn’t included in the income calculations.

The 4 types of Roth conversion strategies are:

- Bracket-Bumping Conversion

- Market-Timing Roth Conversion

- Back-Door Roth Conversion

- Mega Back-Door Roth Conversion

(note: these are strategic approaches—separate from types like standard, in-plan, or IRA-to-Roth conversions).

Want to help your clients go from forever taxed to nearly never taxed?

Contributions to a Roth account are post-tax funds and continue to grow tax-free, so you can keep the government out of your clients’ retirement savings.

When working with clients, be mindful of the tax implications as a whole. It’s common to consider Roth conversion strategies at the end of the year when you have a full understanding of their annual income.

Learn how The Bucket Plan® can help financial advisors increase their profitable business lines.

Let’s dive into each strategy and how to implement them effectively.

1. Bracket-Bumping Conversion

A bracket-bumping Roth conversion strategy attempts to keep converted cash within the client’s current tax bracket, so a conversion doesn’t force any of their funds into a higher bracket.

You can lessen the tax blow and make it more manageable for your clients by spreading conversions across several years to decrease overall taxes.

2. Market-Timing Roth Conversion

The best time to take advantage of a Roth conversion strategy is when the market is down, causing the client’s traditional IRA to lose value.

When account values are temporarily depressed, you can convert more shares for the same tax cost, maximizing the benefit when markets recover.

Sudden market declines may provide a brief conversion window. Time the market so your clients get the most out of their Roth conversion strategies.

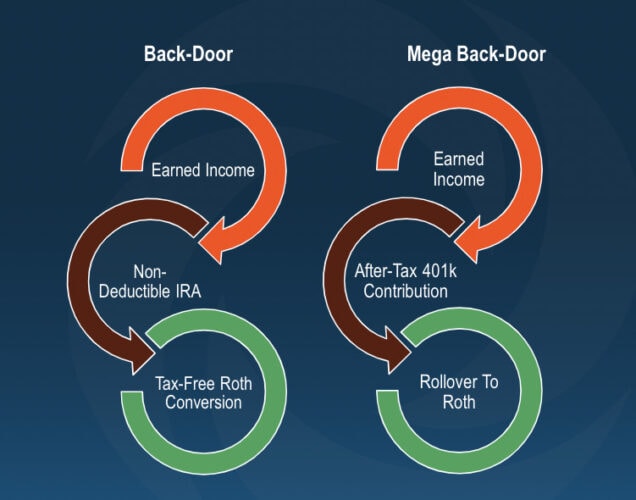

3. Back-Door Roth Conversion

Back-door conversions should be reserved for your high-income earners. This allows clients to utilize a Roth IRA to save for retirement, even if their annual income exceeds the maximum allotted amount.

This strategy works around income limits by contributing to a non-deductible traditional IRA and immediately converting to Roth. There are a number of factors to consider when looking at a back-door Roth conversion, so thorough planning is essential.

4. Mega Back-Door Roth Conversion

Mega-back door conversions should also be reserved for your highest-income earners.

This is where the client contributes after-tax dollars to a traditional 401(k) through their employer. Then, immediately roll it over to a Roth IRA from their 401(k). But don’t forget to consider plan availability and coordination with other retirement savings strategies.

[Related: How to Provide Exceptional Wealth Management for High-Net-Worth Individuals]

A Note About SEP and SIMPLE IRAs

SEP IRAs, SIMPLE IRAs, and traditional IRAs all follow identical conversion rules. Any of these account types can utilize the strategies above. The conversion process and tax treatment are the same regardless of the original account type.

From a conversion standpoint, these accounts are treated as traditional IRAs and can be converted using any of the four strategies that best fit your client’s situation.

2025 Tax Environment Update

Recent tax legislation has made historically low tax rates permanent, creating an unprecedented planning window for Roth conversions.

2025 Tax Brackets (Married Filing Jointly):

| Tax Rate | Single Filers (Income Over) | Married Filing Jointly (Income Over) |

| 10% | Up to $11,925 | Up to $23,850 |

| 12% | Over $11,925 | Over $23,850 |

| 22% | Over $48,475 | Over $96,950 |

| 24% | Over $103,350 | Over $206,700 |

| 32% | Over $197,300 | Over $394,600 |

| 35% | Over $250,525 | Over $501,050 |

| 37% | Over $626,350 | Over $751,600 |

Special Considerations:

- New senior deduction ($6,000 per person over 65) may phase out with higher income

- Enhanced standard deductions provide more tax-free income room

- SECURE Act inheritance rules make conversions more urgent for estate planning

How to Use Roth Conversion Strategies to Manage Taxes

The Tax Management Journey® helps differentiate between tax planning, tax preparation, and tax management.

When you build a house, you first need a blueprint or a plan with everything laid out. This is similar to tax planning, whereas tax management is more like the contractors and builders who get the job done.

And the person who prepares annual tax returns is comparable to an inspector who comes in on a regular basis to make sure nothing is broken, and everything runs smoothly.

Start Putting Tax Management Strategies into Action

Are you optimizing your clients’ portfolios to ensure their taxes are adequately managed and selecting Roth conversion strategies that benefit them?

Book a FREE 20-minute consultation with one of our Business Development Representatives to learn how C2P can help you get started—no tax background necessary!

[Related: How Financial Advisors Can Attract and Retain High-Net-Worth Clients in 8 Steps]

Learn From On-Demand Tax Management Podcasts

Stay up to date with the latest financial planning strategies by subscribing to our C2P podcasts:

The Bucket Plan® On-Demand Podcast

Get insights on comprehensive planning best practices, tax strategies and real-world implementation for serving diverse client needs.

The Rainmaker Multiplier On-Demand Podcast

Hear how top advisors build scalable practices using proven tax management strategies and holistic planning approaches.

Financial Professional Use Only

- The information provided in this presentation is not intended as investment advice or legal advice.

- The information provided is for informational and training purposes only.

- The information in this presentation was accurate as of the time of the material was created.

Tax laws and rulings can frequently change. Please discuss the client’s current situation with an accountant or tax advisor.